#293: Gaming Trends in 2024 (So Far!)

🎮 Where is web3 gaming now and where is it headed?

TPan here! I’m still on the third leg of my honeymoon so I won’t be writing my usual pieces. However, I do have some great content for you from others in the space.

This essay is drafted by Colleen Sullivan, Co-Head Venture at Brevan Howard Digital, and Alex Matthews and Ross Trachtman, both Principals with the Brevan Howard Digital venture team. Colleen has written previously on the intersection of web3/gaming and Colleen, Alex, and Ross all spend a significant amount of time investing in this area. On X/Twitter, you can find the team at: Colleen (@colleenklein), Alex (@alexmatthews95), and Ross (@cryptoscoe) and on LinkedIn at: Colleen, Alex, and Ross. Nothing in this essay is endorsed by Brevan Howard Digital and/or any of its affiliates. Please see the disclaimer at the end of this essay.

The Tremendous State of web3 Gaming in Q1 2024 & the Troubled State of web3 Gaming 30 days into Q2 2024

When we initially read Matthew Ball's magnificent opus, The Tremendous Yet Troubled State of Gaming in 2024, we thought this to ourselves:

As Ball describes in his essay, while web2 gaming is massive in terms of gamers (3.38 billion 2023) and revenues ($184 billion 2023), the industry is facing some equally massive headwinds (all stats from Ball’s essay unless otherwise noted):

Layoffs:

2022: 8,500 (record)

2023: 10,500 (new record)

By the end of February 2024: 8,500, which doesn't include 8% layoffs at Microsoft and Sony; 5% layoffs at EA and Take Two; and 11% layoffs at Riot

Stalled Growth:

In real (not nominal) terms, US gaming revenues in 2023 are 2.1% under 2022, 14.3% under 2021, 13.6% under 2020, and up only 6.9% from 2019

According to Newzoo’s PC & Console Gaming Report 2024, on PC / console, average quarterly playtime has decreased by 26% since Q1 2021

According to Unity’s 2024 Gaming Report, in-app purchases are driving less overall revenue than they did in 2022; IAP ARPDAU is down 13%

Continued IDFA/ATT Fallout: Mobile gaming downloads peaked during Q1 2021, the quarter before Apple introduced its IDFA/ATT policy changes and show no signs of recovering. The mobile gaming market in 2023 saw a 10% decline in downloads year-over-year, largely due to rising user acquisition costs, highlighting the challenge publishers faced in connecting with target audiences post deprecation of IDFA.

It's Hard for Games to Breakthrough:

Mobile:

In the US, the top three mobile games per genre generate ~40% of the genre’s revenue (range of 20-90%)

82% of revenue is derived from titles over two years old (and over 50% is generated from titles over four years old)

The top three shooters are 70% of revenue and titles over 2 years old are 94% of that

PC / Console:

Games ranking in the top 10 by average MAU are over seven years old on average and generally fall into one of four categories

66 titles accounted for 80% of playtime in 2023, in line with the trend of the last two years

Games that are at least six years old accounted for more than 60% of playtime in 2023

14,531 games were released on Steam in 2023 or ~40 games / day, making discoverability of/attention on new games very challenging

Of those 14,531 new games: (i) the top 100 accounted for 91% of full game revenue from 2023 releases and (ii) only ~700 (5%) made over $100,000 in full game revenue

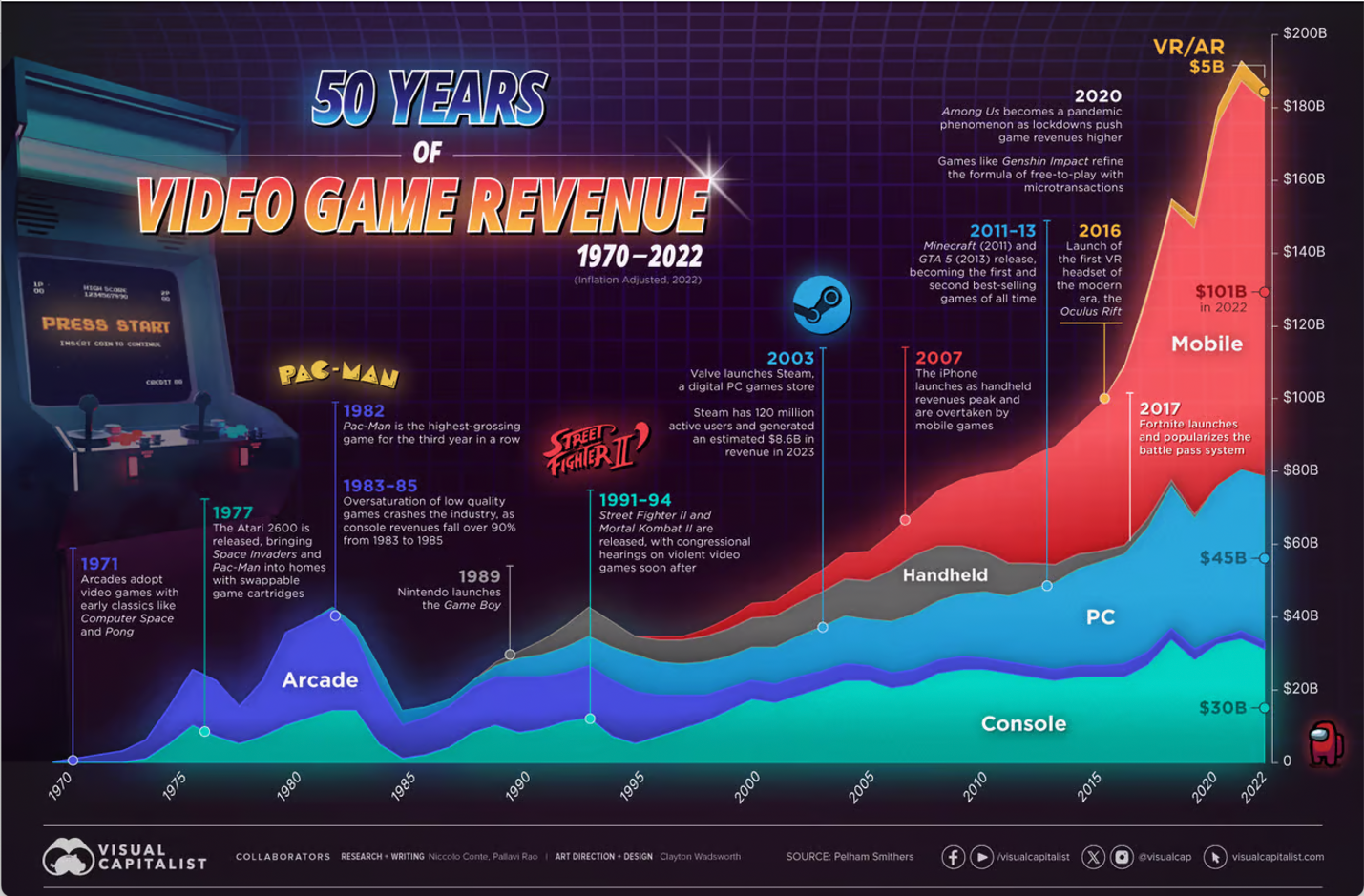

As the above data indicates, mobile, PC, and console gaming are all looking increasingly ossified. So, how does gaming get back to a growth state? As the below graphic (1) shows, gaming generally shifts into a growth state when new mediums or platforms are introduced. As readers who are familiar with our work know, our thesis has been (and continues to be) that the clearest way to get gaming growing again is to expand the gaming market with a new medium — which we believe is the integration of web3 technologies in games — because this leads to net new monetization opportunities.

We can use the proxy of transaction volume to approximate just how early we are in the monetization opportunity for web3 gaming in the broader gaming landscape. According to DappRadar, the top 20 web3 games accounted for $498 million in volume (2) in the past 30 days. Annualized this equates to ~$6 billion, or ~close to VR/AR in the above chart. Assuming 1% to 10% of the volume is revenue, we arrive at an estimate of between $60 million and $600 million in revenue. Now, there are 900+ blockchain games and this is one crude and very conservative estimation. Many of these games have NFTs / digital objects which have done significantly more volume and some of these games also generate traditional IAP and IAA revenue, but the point is to show that current revenue is a drop in the bucket compared to what it will be in a decade. We believe that the ability to add web3 technology to games is the onset of a new medium that will expand the revenue opportunity in gaming (we’ve written extensively about this). And as you can see below, some of the largest web2 gaming companies in the world also see this opportunity and are currently adding web3 technologies to their games (more on this below). To give you a sense of how big some of these companies are, we’ve added approximate 2023 revenue figures (3)(some are CY2023, some TTM, some are closest FY):

*Zynga was acquired by Take Two in May 2022, the revenue figure is for the combined entity

**CCP Games was acquired by Pearl Abyss in 2018

Q1 2024 web3 Gaming

Throughout Q1, web3 gaming related companies/projects continued to raise capital, albeit at a similar rate to Q1 2023 and far below the Q1 2022 mark. From Jon Jordan’s Big Blockchain Game Report Q1 2024:

The first three months of 2024 saw 68 investment deals in the blockchain gaming sector, down 1% compared to Q1 2023 and down 57% compared to the boom times of Q1 2022, in which 56 deals were announced in March 2022 alone

In Q1, there were 166 new blockchain games (Jordan maintains a “Big Blockchain Game List”, which is a fantastic resource and linked here)

Some of the newly added games are live and some are in development, but the pace isn’t slowing down. Further, public comps (tokens which are already live and trading) have trickled into private market valuations, and live tokens have incentivized private tokens to launch at all costs while the window of opportunity remains open. Further, nearly all of the top gaming tokens were in the green and new gaming token listings continued to ramp up:

In sum, Q1 2024 for web3 gaming was awesome! And if TPan asked us to publish this piece on March 31, 2024, our opening meme would have held up! But, alas, we're publishing on May 2, 2024 and this being web3 and all — where narratives go to die quicker than Google Stadia — the appropriate opening meme for the current state of web2 gaming and web3 gaming one month into Q2 2024 is more like:

Q2 2024 web3 Gaming (...first 30 days)

The start of Q2 has been a bloodbath for alts and gaming is no exception:

According to TradingView’s altcoin market capitalization index, valuation peaked at $350 billion on March 24, 2024 and dropped to $245 billion as of April 30, 2024

Major projects such as Lido and Arbitrum are both down over 30%+ despite real and significant traction

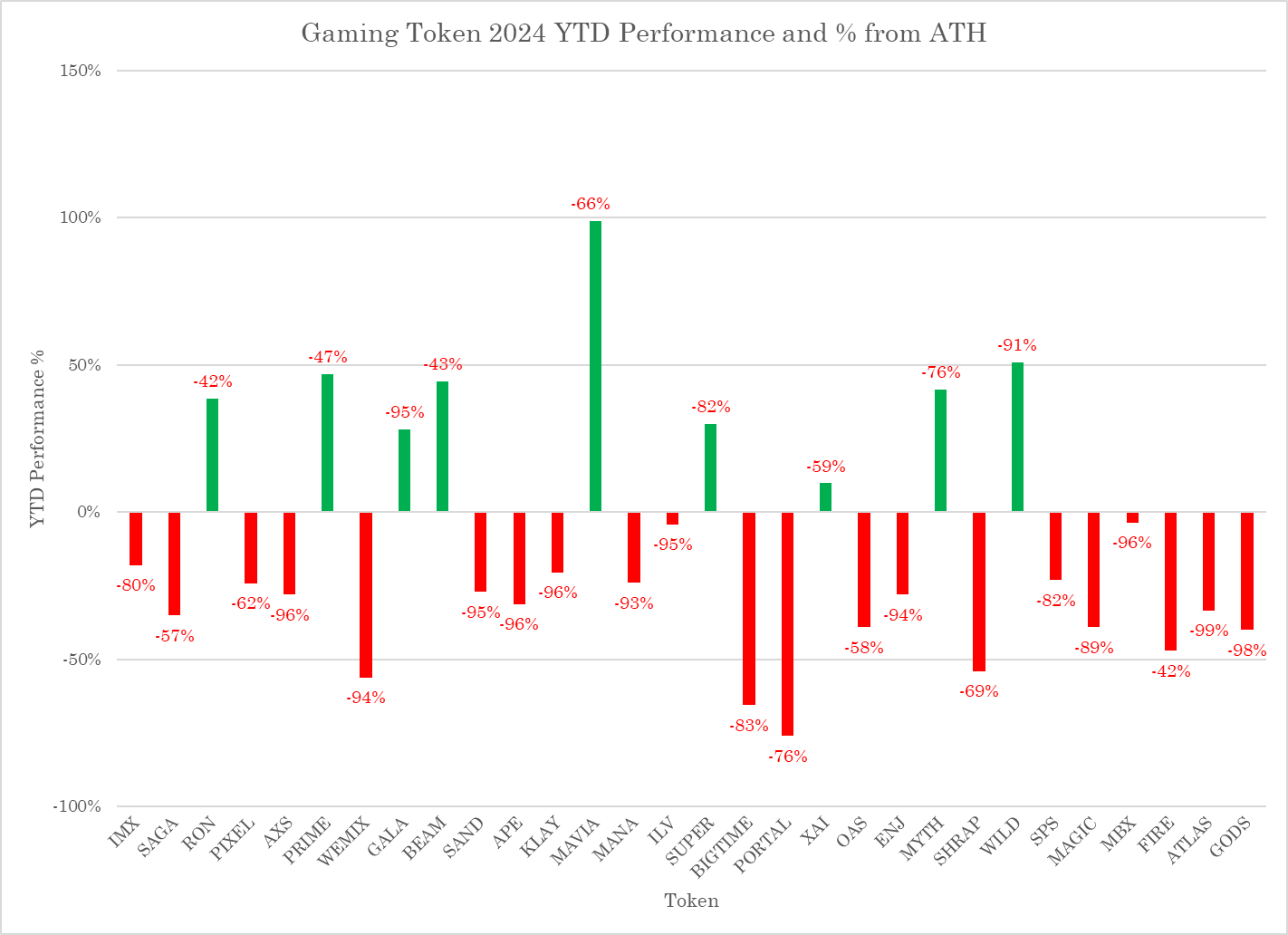

In our analysis of the top 30 gaming tokens, only seven had not appreciated in Q1 2024, but when you add in April, only nine remain in the green with 21 in the red

All top 30 gaming tokens — regardless of launch date — are currently over 40% below their ATHs

We mentioned above that we’ve seen web3 gaming projects pushing to launch tokens while the “window of opportunity remains open” but what if that window is already closed? While we certainly hope that isn’t the case (and we don’t think it is), when we looked at the performance of new gaming token listings (4) across Q3 2023 to April 30, 2024, we got the following:

It’s obvious from the number of token listings in each quarter that gaming projects have chased the market with a clear acceleration in listings in Q1 2024 and the start of Q2 2024. Inevitably, many projects took the opportunity of favorable market conditions and exchanges’ greater propensity to accept new IEO listings (given the significant fees generated by heightened volume on new launches) to push their tokens to market. What’s also clear from to-date performance is that tokens listed in Q3 2023 —prior to much of this crypto market bull run — have performed the best and held their value despite the wider market pullback in recent weeks. Unsurprisingly, listing publicly towards the end of the bear market just before a bull cycle arrives appears to offer the best chance of success if measured by token price appreciation. In contrast, projects that entered the crypto public markets after Q3 2023 show markedly worse performance, which we believe may be attributable to a combination of factors, including:

Many projects launched with low circulating supply and heavy airdrop campaigns. While airdrops can be effective UA tools for users with real LTVs, they also draw a crowd of extractors that have no plans to engage with the game over a longer time horizon.

In the early months after launch, it's often the case that the primary holders of unlocked tokens are airdrop recipients (team members and investors are typically locked up when a token launches). When wider markets are in distress, these holders can be quick to take profits on their free airdrop, which can lead to poor token performance.

We’ve seen this happen with projects like Portal, which currently has ~16% circulating supply, driven primarily by airdrop recipients and launchpad stakers. Portal launched at ~$3.25 billion FDV when it listed on February 29, 2024 and is down ~76% as of April 30, 2024 (5).

Some projects simply missed out on much of the hype cycle around gaming tokens in Q4 and Q1 and bore the brunt of the brutal alt sell-off in recent weeks.

Retail investors/traders may be feeling burned because gaming projects with a lot of frenzy, including significant KOL shilling, haven’t performed as expected and now those same investors/traders are backing off as they search for more substance beneath the surface.

So, while web2 gaming is clearly going through a challenging time, it’s not all sunshine and rainbows here in web3 gaming either. Additionally, web3 game developers have a different and unique set of considerations to contend with:

Within the last ~4 weeks, many of the top game developers and infrastructure providers in this space saw the public facing values of their projects drop 20-50%+, e.g.:

On March 11, 2024, Immutable’s token ($IMX) was trading at $3.69 and on April 30, 2024, it traded at $1.87, a drop of 50%

On February 25, 2024, Sipher ($SIPHER) was trading at $0.80 and on April 30, 2024, it traded at $0.26 on April 30, 2024, a drop of ~68%

The upside of early community and gamers getting direct exposure to their favorite games does not come without peril; sentiment can switch on a dime and the contrast of the last few weeks with Q1 is a painful reminder of this.

Further, even in the vertical of gaming (an application), infrastructure remains king. The top 30 gaming-related tokens by FDV are overwhelmingly dominated by infrastructure-focused projects. These tokens hold significantly higher FDVs compared to content/IP. Single-title gaming tokens — aside from exceptional outcomes like Axie and Pixels — overwhelmingly trade at valuations under $1 billion. Many of the highest valuations in this single-title category are artificially inflated by low circulating supplies as can be seen in the following table (6):

It follows that many content/game developers have turned to developing some facet of infrastructure. For some projects, this is development tooling to build web3 games. For others, it’s a layer 1 or layer 2 for other developers to deploy their games on. Examples here include Shrapnel (7) and Parallel, which recently announced Mercury and Colony, respectively. This does make some sense; web3 gaming is still so nascent that additional tooling is needed and who better to build those tools than the studios dogfooding it? Further, game developers often seek some sovereignty when building their stack/gaming environment. In fact, it’s currently challenging to find a gaming project/corresponding token that doesn't have some sort of infrastructure component. As Munger would say, “show me the incentive, I’ll show you the outcome.” It remains to be seen if/when this changes. One would hope that web3 game developers who attract, and bring joy to mass audiences around the world, will be rewarded commensurately. Maybe that finally happens when the state of infrastructure is solid and comprehensive enough (8) that developers no longer need to — or are incentivized to — focus on that part of developing web3 games.

Also, while content and infrastructure are two critical components in the business of games — distribution remains king. We won’t rehash our prior thoughts here, but to onboard the proverbial billions of gamers to web3, we also need traditional game distribution channels like the Apple App Store, the Google Play Store, Steam, Xbox, and PlayStation to welcome web3 games with open arms like the Epic Games Store (so far) has done. We also expect web3 gaming to generate sufficient network effects over time that result in distribution innovations bespoke to blockchain based games/the web2 and web3 gamers who enjoy these games.

Trends in Q1 2024 web3 Gaming

web3 gaming x AI

Much has been made of AI’s potential impact on creative industries and gaming is no different. While many focus on generative AI disintermediating aspects of the production process, headlines this quarter in web3 gaming x AI have centered around AI NPCs’ involvement in games with real-value tokens. Parallel’s newly announced title, Colony, has prompted (pun intended) more focus on the ways that crypto and AI will transform the gaming industry. In the case of Colony, two whitepapers were published – one for Colony and one for Wayfinder, an AI protocol that underlies the game. This also accentuates the theme discussed above, whereby game studios in web3 focus on a piece of infrastructure alongside the games they develop. Other developments in this category are Ultiverse’s raise, which is another game publisher looking to build tooling around smart agents.

More broadly, it’s inevitable that AI will transform all aspects of the gaming industry from the very beginning stages of production all the way to live ops. Indeed, from Unity’s 2024 State of Gaming Report:

“62% of the studios we surveyed said they used AI in their workflows, mainly to prototype quickly and for concepting, asset creation, and worldbuilding.”

We think the use of AI is even more interesting in web3 gaming where some or all the aspects of a game are on-chain. Provably fair becomes even more important in a world where NPCs can interact with the state of the game in an evergreen fashion or in a world where they trade NFTs with real value in a marketplace.

Fully Onchain Games (FOCGs)

Another area where we saw increased activity in Q1 is fully onchain games (FOCGs). As you may have noticed above, we stated that “some of the largest web2 gaming companies in the world ... are currently adding web3 technologies to their games.” (9) Let’s take a quick detour and clarify what we mean when we say "adding web3 technologies to their games.”

Some of you probably play Pokemon Go, one of the most popular video games in the world. Let's assume that Pokemon Go's developer Niantic decides to add web3 to Pokemon Go. Niantic would then issue the Pokemon as NFTs and secure them on a decentralized blockchain like Ethereum. The effect of this is that you would actually own your Pokemon and be able to sell them if you wanted to. Many gaming companies are doing exactly this and that's what we mean when we say "adding web3 technologies to their games."

But these games aren't FOCGs because they don't have the entirety of their game state and game logic running on a blockchain. In FOCGs, every change to the state of the game must be recorded to the blockchain — every score update, every character movement, every turn taken. In our example, Pokemon Go's game state and game logic are created and maintained on a centralized third-party game engine called Unity and secured by Niantic's centralized servers. If Niantic goes bankrupt, bans gamers, or loses its license with Nintendo to use the Pokemon IP, gamers instantly lose access to the game they love and their in-game community of friends.

If Pokemon Go were a FOCG, Niantic could disappear entirely and Pokemon Go would still be accessible by anyone when they connect to the public blockchain Pokemon Go is built on. In fact, this very problem in a game called World of Warcraft is one of the reasons Vitalik Buterin created Ethereum.

Thus far in web3 gaming, we’ve dedicated the lion’s share of capital, development, and attention to building web2 games with item ownership and/or the financial aspects of the game on blockchain rails.

The first step to building FOCGs is to build fully onchain game engines. All games require game engines (10) and, for frontend game engines, most game developers use one of two prominent third-party game engines: Unreal, which launched 26 years ago, and Unity, which launched 19 years ago. Given how old these game engines are, it's probably clear that web2 frontend game engines and blockchains are not specifically designed for each other and getting them to talk to each other gets very complicated, especially as more and more components of a game are put onchain. Additionally, blockchains aren't yet ready to put AAA games fully onchain due to the significant number of inputs per second required in those games. For context, Monopoly Go does 2.1 million database writes per second and, although today’s blockchains are making super impressive gains in scalability (yay Firedancer!), they’re not yet ready for that number of inputs per second. As a result, there are fewer projects that choose this path. In fact, from Jordan’s list above, only 71 of the 953 blockchain games he tracks are categorized as FOCGs.

We are optimistic that this category, while nascent, is meaningfully differentiated. As illustrated in our Pokemon Go example, a FOCG is trustless, and players can take comfort that no centralized entity will alter their financial assets or gameplay in a way that is harmful. Early experiments from an investor’s perspective are promising; while FOCG user bases are miniscule compared with web2 or even web2.5 games, the user behavior is markedly different.

We’ve also seen talent begin to dive into the FOCG category, with some of the brightest gaming and crypto minds devoting time to this area (check out our portfolio company, Turbo!). Over time, the scalability issue will be solved as will the accessibility issue for both developers and users.

Multiplatform / Multichain

One other trend we're keeping a close eye on is blockchain games releasing multichain versus single chain. Jordan notes in his Q1 report that of the 119 new blockchain games released in Q1, 27% launched multichain (and out of 953 existing blockchain games, 21% are multichain). In Jordan’s data we see single games launching multichain on Solana and Base and on Oasys and Polygon. With respect to the former, those chains require different developer coding skillsets and the appeal of launching a Solana based game on Base is likely the ability to distribute the game to Coinbase's 100 million users (remember, distribution is king). With respect to the latter, one reason game developers may want to launch a Polygon based game on Oasys is to better access gamers based in Japan, where the Oasys team is based (further, many of Oasys' validators are large web2 gaming companies like Sega, Bandi Namco, and Square Enix). This is logical because right now, the web3 gaming player base and their liquidity is fragmented across chains.

History doesn't repeat, but it does rhyme. Launching a web3 game multichain is somewhat analogous to launching a web2 game multiplatform. Prior to Fortnite, Sony refused to support cross-platform play so if your friends all had Sony PlayStations and your parents bought you a Microsoft Xbox for your birthday, you were out of luck and had to game alone. In 2017, Fortnite "accidentally" enabled cross-platform play between PlayStation 4 and Xbox One and while Fortnite quickly remedied this "error," the secret was out — now gamers knew cross-platform play was technically possible and that Sony had been intentionally maintaining its private walled garden. Fortnite players mounted a strong campaign for cross-play, forcing Sony to yield after a year. Sony finally bending the knee opened up Fortnite cross-platform gameplay, progression, and commerce across PlayStation 4, Android, iOS, Nintendo Switch, Xbox One, Windows, and Mac. Why does this matter? Epic Games, the creator of Fortnite, found that increased cross-play engagement has a big impact on monetization — the average monthly revenue-per-user who cross-played Fortnite was 365% higher than non-cross-players. Further, cross-players played Fortnite 570% more on average than non-cross-players. Keeping those stats in mind and fast forwarding to today, it's no surprise that:

Unity's 2024 state of gaming report found that:

in 2023, 95% of studios with 50+ people prioritize cross-platform play

there has been a 34% increase in games launching on three or more platforms between 2022 and 2023

55% of studios surveyed are starting to plot their multiplatform strategies during preproduction

Newzoo’s PC & Console Gaming Report 2024 found that nearly half of players (47%) play on two platforms or more and that players who engage with more platforms tend to invest more time and money into gaming. This means that expanding beyond a single platform can provide more routes to reach attractive and potentially lucrative player groups.

It's useful to keep in mind that solving web2 cross platform play wasn't simple and tools needed to be built to handle, without limitation: cross play functionality (networking, matchmaking, and communication across different platforms to seamlessly play together); input handling (adapting to different input methods, e.g., controller, keyboard/mouse, touchscreen); performance optimization (accommodating a wide range of hardware to ensure smooth gameplay from high-end PCs to mobile devices); graphics and UI (scaling visual elements and interfaces to adapt to various screen sizes and resolution); shared account services (unified system for players to maintain a single account and friends list across platforms); social features (lobbies, voice chat); cross-platform synchronization (keeping game states, player progress, player achievements, and other data in perfect sync across different systems); anti-cheat; and analytics and data storage (systems to collect player data and game metrics and analytics to understand player behavior in aggregate across platforms).

We're aware of all the "problems” in launching multichain games today including, without limitation: bridging/interoperability, composability, wallet integrations, security, governance, needing multiple (expensive) developers with skillsets across differing ecosystems (e.g., solidity, rust, move, etc.). Another “difficulty” in deploying games cross chain is that if a game studio accepts a grant from a blockchain ecosystem foundation, the terms of the grant often require exclusivity to that blockchain ecosystem for a certain period of time (not all that dissimilar to Sony’s PlayStation exclusivity deals). Finally, bespoke cross chain challenges arise if a game is a FOCG versus solely issuing its assets/economy onchain.

Ultimately, the advent of cross chain intent infrastructure and chain abstraction should take us to a place where web3-enabled games need only select the best chain for their economy/assets to be primarily deployed on. In this world, users with cross-chain enabled wallets should be able to access a game that’s located on any chain regardless of what chain that user spends most of their time on or where that user holds most of their assets. There are various approaches to this chain abstracted outcome, and the layer (11) to achieve this should take shape over the next year or two. This should obviate the need for games to deploy their economies across multiple chains because they will be able to access all users that have engaged with web3 regardless of their chain preference (12). As far as user acquisition goes, the future of web3 gaming should develop to the point where users find games via traditional means (or their web3 analogs), and players spend time and money in games because they enjoy them, not because they’re on a specific chain.

If siloed, private walled garden platforms ultimately didn't make sense in web2 gaming, it’s really unclear why siloed, private walled garden chains would make any sense in web3 gaming — where the foundation of the industry resides on systems "based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party." As we've written before, gaming is a social experience — indeed, we believe gaming is the next evolution in communication itself — and gamers’ social graphs should not be limited by artificial social boundaries like platforms or chains. Gamers should be able to game with their friends regardless of what chain, e.g., Solana, Base, Arbitrum, Immutable, Telegram or device, e.g., PlayStation, Xbox, mobile, PC they happen to be on. Further, the lesson learned in web2 is that games monetize best when they sit in the hands of as many gamers as possible irrespective of what device or medium gamers happen to be using. And, just as the technical (and practical, e.g., exclusivity deals) challenges of cross-platform gameplay were gradually overcome, the complexities of multichain gameplay will likewise be solved, primarily through the type of innovation described in the above paragraph.

Why Can't We be Friends?...maybe we already are?

Notwithstanding the April 2024 carnage, we remain as optimistic as ever on the future of web3 gaming. In fact, we think the last 30 days have largely been positive for the space. Some of the peak froth from 2021 was seeping back in, e.g., hundred million+ seed stage valuations and promises of $1b+ in revenue and 100 million+ MAUs within one year of game launch (which are difficult metrics for even the best of AAA web2 games to achieve!). Hopefully this pullback washes out some of the opportunists that rushed in as soon as prices started going up at the end of last year. While volatility is a feature, we're at the stage where it's much more important to keep showing why web3 technologies deserve a seat at the gaming table. And on that note, we were happy to see in Konvoy's Gaming Industry Report Q1 2024 that venture funding was up 94% QoQ and number of rounds were up 28% QoQ and that tech, platforms, and game studios using web3 technologies materially contributed to those figures. Specifically:

of the largest gaming tech and platform VC deals, web3 related deals numbered seven out of 10 deals, representing $56.4 million in funding out of $76.6 million in total funding

of the largest game content VC deals, web3 games again numbered seven out of 10 deals representing $203 million in funding out of $333 million in total funding

Is this an early indication that “web3 gaming” is just becoming “gaming”? Maybe. But one thing those stats make us feel good about is ending this essay with what we believe the future state of both web2 gaming and web3 gaming really looks like:

Annotations

https://www.visualcapitalist.com/video-game-industry-revenues-by-platform/

The fiat value of incoming token transfers from unique active wallets (UAW) to the dapp’s smart contracts over a period of time.

Figures were taken from public filings where applicable, in addition to Bloomberg, Yahoo Finance, and news outlets such as TechCrunch, Reuters, Financial Times, Businesswire, Gamesindustry.biz. Some figures are CY2023, some TTM, some are closest FY to CY2023.

These are unique primary listings across Binance, Bybit, Kucoin, Huobi, Kraken, OKX and Coinbase.

Circulating supply, valuation and performance retrieved from CoinGecko.

Table showing valuations and circulating supply of the top 30 gaming-related tokens with data from CoinGecko.

Shrapnel is a AAA game produced by Neon Machine, a Brevan Howard Digital portfolio company.

Our portfolio company, Sequence, is working hard to make this happen!

Note that many games that add web3 technologies to their games also issue a fungible token.

There are frontend and backend game engines, but getting into the details of game engines and how they work is beyond the scope of this essay.

e.g., with fast bridges, with a chain abstraction SDK for game developers, with a cross chain wallet, etc.

These games could still choose to launch their assets on their non-home chain (making them transferable, cross-chain assets) as a distribution/marketing tool to increase their monetization capabilities.

Resources

We read and listened to a lot of great and/or thought provoking gaming related content so far in 2024 — here are some pieces that stood out:

MapleStory Universe GDC 2024 Session Full Script

The Tremendous Yet Troubled State of Gaming 2024 (Matthew Ball)

On Spatial Computing, Metaverse, the Terms Left Behind and Ideas Renewed (Matthew Ball)

Arbitrum Gaming Catalyst Open Draft

Why Shrapnel is leaning into the “early” in Early Access

LinkedIn plans to add gaming to its platform

2024 For Japanese Companies (Naavik Research)

The State of UGC Games (2024) (Naavik Research)

What’s Next for Tencent (Naavik Research)

Where Gaming Meets AI (Naavik Research)

Steam’s Top 10 Games Captured over 60% of Revenue in 2023

Chinese Game License Approvals Surpassed 1,000 in 2023 in Return to Form

Banking on Video Games and Virtual Worlds (report issued by the US Consumer Financial Protection Bureau)

The Backend Game Jungle: A Short Guide for Game Executives

Unity Sees WebGPU as a Growing Market for Game Development

Apple Lifts Ban for Game Emulators on iOS

For Schell Games, VR is the technology of the present (possibly the future, too)

Ubisoft Returns to web3 Gaming

Why it's become harder to raise investments in mobile game development in 2024

The Pitfalls of Multichain Strategies for web3 Games (Immutable)

A New Era for Mixed Reality (Meta)

Opening Up Marketplace to More Creators (Roblox)

Analyst Bulletin: Mobile Game Market Review March 2024

OnChain Report 2024 (QuickNode x Artemis)

Jon Jordan’s web3 Gaming Substack (every post)

Stephen Totilo’s web2 Gaming Substack, Gamefile (every post)

Dark Tunnels & WASD: our go to sources for FOCGs

Games Fray: our favorite source for all things related to Epic’s battles with Apple / Google + EU DMA

Gamecraft: The State of Play 2024

Deconstructor of Fun (all episodes)

Naavik Gaming Podcast (all episodes)

Important Legal Information and Disclaimer

The commentary contained in this document represents the personal views of its authors, Colleen Sullivan, Alex Matthews, and Ross Trachtman, and does not constitute the formal view of their employer or its affiliates. It does not constitute investment research. The views expressed in the document are not intended to be and should not be viewed as investment advice. This document does not constitute an invitation, recommendation, solicitation, or offer to subscribe for or purchase any securities, investments, products or services, or any investment fund. Unless expressly stated otherwise, the opinions are expressed as of the date published and are subject to change. No obligation is undertaken to update any information, data or material contained herein. This document is issued by Colleen Sullivan, Alex Matthews, and Ross Trachtman in their personal capacities.

As the broader gaming industry gradually shifts its focus to blockchain, web3, and crypto, we’re going to see these themes play out and grow.

On X/Twitter, you can find the team at: Colleen (@colleenklein), Alex (@alexmatthews95), and Ross (@cryptoscoe) and on LinkedIn at: Colleen, Alex, and Ross.

See you soon!